Title insurance is unlike any other kind of insurance coverage. While most insurance policies are protecting against future risks, a title policy provides protection from the consequences of past events. And unlike other types of insurance, you make only one premium payment for a lifetime of coverage.

Title Insurance Protects Your Right of Ownership

Title insurance protects the title – which is the legal document evidencing a person’s right to or ownership of a property — to a property from legal challenges that might arise before the property was purchased.

What Title Insurance Protects Against

Title insurance protects against losses due to defects in a property’s title, such as liens, encumbrances, and prior recorded mortgages. It also protects against claims or prior rights that other parties may have to the property.

How Title Insurance Works

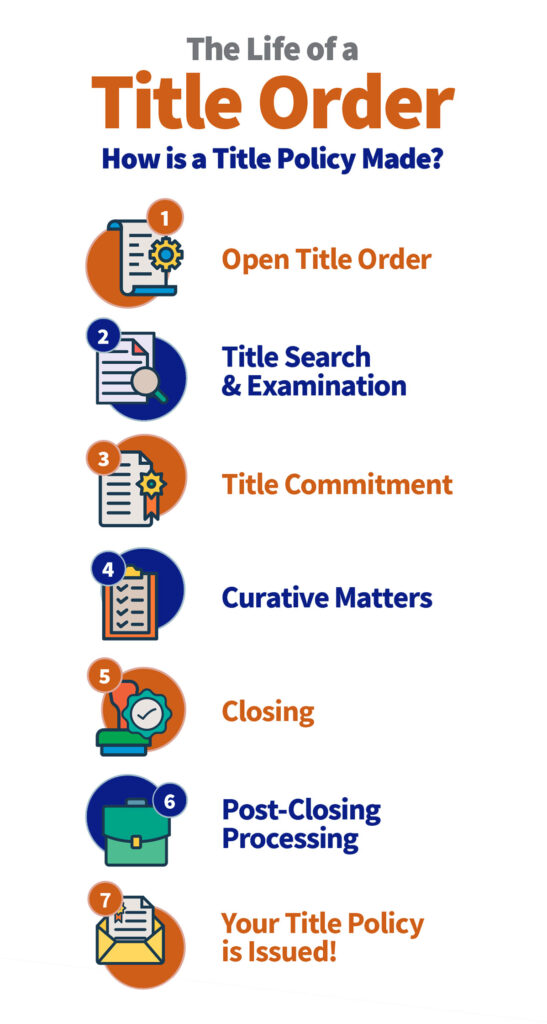

Title insurance is based on a public records search that determines the state of the title at the time of purchase. If someone challenges the title, the title insurance underwriter will defend the title and pay any related costs.

How Title Insurance Differs From Other Insurance

Title insurance is different from homeowners insurance and other casualty insurance because it provides protection for an indefinite period of time from future losses due to events that have already occurred.

Two Types of Title Insurance Policies

Anyone who has a financial interest in the property should have title insurance. On most residential properties, there are two parties who should have coverage: the lender and the homeowner.

The lender needs protection only for the amount of the loan. The homeowner should also have an owner’s policy for the purchase price of the home. Anyone buying a home should discuss this with their attorney. Ask whether or not it makes sense to add a survey endorsement or an inflation rider to the owner’s policy. Be sure to read the title commitment before the policy is issued to find out what restrictions apply.

Common Title Defects

If the title of a property is checked to be ‘clear’ each time the property transfers from one owner to another, why is title insurance required by lenders and recommended for anyone buying a property? That is because there are common hidden risks that can cause a loss of title or create an encumbrance on title:

- Instruments (documents) executed under invalid or expired power of attorney

- Undisclosed or missing heirs

- Mistakes in recording legal documents by municipal or county government

- Misinterpretations of wills

- Deeds by persons of unsound mind, by minors or by persons supposedly single, but in fact married

- Fraud

- Liens for unpaid estate, inheritance, income or gift taxes

- Forged deed, releases or wills

Title insurance protects the purchaser of the property from claims arising from any one of those events if the event took place before the property was purchased.